Have you ever felt like you’re working harder and harder but not getting ahead financially? Do you aspire to escape the monotonous routine of your day-to-day work and attain genuine financial freedom? If so, you’re not alone. Many people find themselves stuck in a cycle of trading time for money, wondering if there’s a better way.

The good news is, there is. Robert Kiyosaki, the author of the bestselling book Rich Dad Poor Dad, introduced a powerful concept in his follow-up book, The Cashflow Quadrant. This framework provides a roadmap for understanding how money works and how you can shift your mindset to achieve financial freedom. Let’s understand the 7 key takeaways from Robert Kiyosaki’s Rich Dad Cashflow Quadrant.

In this blog post, we’ll dive deep into the Cashflow Quadrant, exploring the four types of income earners and how you can transition from being an employee or self-employed to becoming a business owner or investor. Whether you’re looking to escape the rat race, build wealth, or create passive income streams, this guide will provide you with the insights and strategies you need to take control of your financial future.

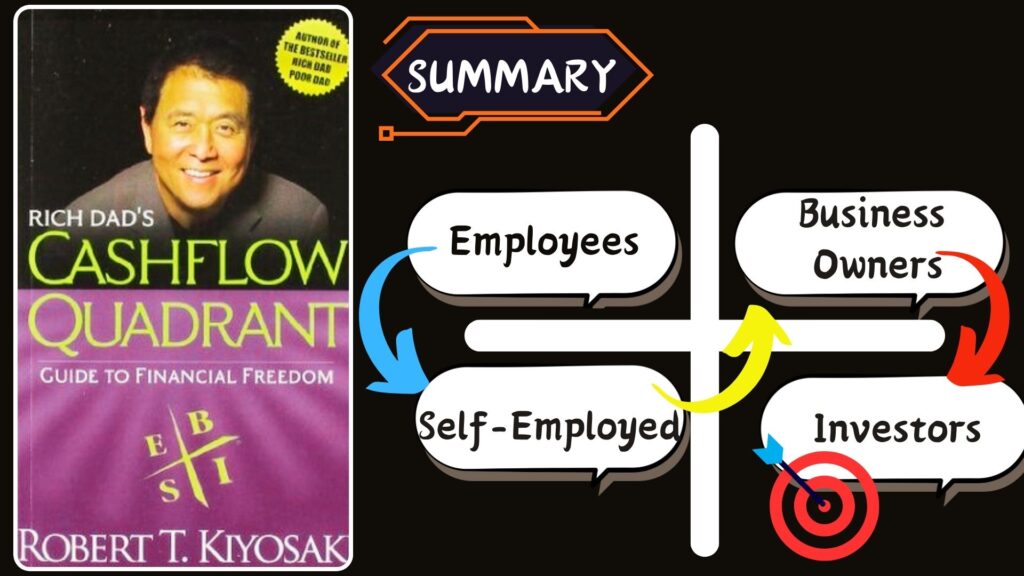

What is the Cashflow Quadrant?

The Cashflow Quadrant is a simple yet profound framework that categorizes income earners into four groups:

1. Employee (E): 1. Employee (E): You are employed by another person or company and exchange your time and effort for a salary or wages.

2. Self-Employed (S): You work for yourself, but you’re still trading time for money.

3. Business Owner (B): 3. Business Owner (B): You control a system or enterprise that produces income, allowing you to earn even without direct daily involvement.

4. Investor (I): Your money works for you, creating passive income and building wealth.

Assessing where you currently stand on the quadrant is the first step toward reaching financial success. The goal is to transition from the left side of the quadrant (E and S) to the right side (B and I), where your income is no longer tied to your time.

Let’s explore each quadrant in detail.

The Employee Quadrant (E)

The majority of people begin their professional journey in the Employee quadrant. As an employee, you exchange your time and effort for a fixed income. While this provides a sense of security, it also comes with limitations.

Pros:

– Steady income.

– Benefits like pension, gratuity, health insurance and other retirement plans.

– Clear job responsibilities.

Cons:

– Your earning capacity is restricted, as your income is limited by a fixed salary.

– Lack of control over your time.

– Vulnerability to layoffs or economic downturns.

Kiyosaki emphasizes that while being an employee is a great starting point, it’s not the path to financial freedom. Creating real wealth requires a mindset shift and venturing beyond your current quadrant.

The Self-Employed Quadrant (S)

This quadrant covers professionals like freelancers, consultants, and entrepreneurs running their own small ventures.

While you have more control over your work, you’re still trading time for money.

Pros:

– Greater autonomy and flexibility.

– Potential for higher earnings than a traditional job.

– Ability to pursue your passions.

Cons:

– You’re still tied to your work (if you don’t work, you don’t earn).

– Risk of burnout from long hours.

– Scalability is limited—your income rises only as much as your direct effort allows.

Many self-employed individuals find themselves working harder than ever, only to realize they’ve created a job for themselves rather than a sustainable business.

The Business Owner Quadrant (B)

Financial independence truly takes root in the Business Owner quadrant. Business owners create systems and teams that generate income, even when they’re not actively involved.

Pros:

– Scalability (your income isn’t limited by your time).

– An owner can delegate tasks to employees and make use of their skills and expertise.

– Potential for significant wealth creation.

Cons:

– Requires upfront effort to build systems and teams.

– Early-stage challenges may include financial losses or business failure.

– Requires competent leadership and management skills.

Kiyosaki stresses that the key to success in this quadrant is creating a business that can run without you. This allows you to enjoy the fruits of your labor while pursuing other opportunities.

The Investor Quadrant (I)

The Investor quadrant is the pinnacle of financial freedom. Investors make their money work for them by acquiring assets that generate passive income.

Pros:

– More income streams (income that flows without your active involvement).

– Ability to grow wealth exponentially.

– The liberty to dedicate your time and energy to the things that hold the most significance in your life.

Cons:

– Requires financial education and discipline.

– Risk of losing money if investments are poorly managed.

– Need for initial capital to get started.

Kiyosaki emphasizes the need to clearly differentiate between assets and liabilities. Assets build long-term wealth and on the other hand liabilities may degrade your financial position. By focusing on acquiring assets, you can build lasting wealth.

How to Transition Between Quadrants?

Moving from the Employee and Self- Employed sides of the quadrant to the Business Owner and Investor side requires a dedicated knowledge and change in mindset. Below given are some tips to help you make the transition:

1. Educate Yourself: Learn about personal finance, investing, and business systems.

2. Start Small: Begin investing in assets, even if it’s just a small amount.

3. Build a Network: Surround yourself with like-minded individuals who can support and inspire you.

4. Create Systems: If you’re transitioning to the Business Owner quadrant, focus on building systems that allow your business to run without you.

7 key takeaways from Robert Kiyosaki’s Rich Dad Cashflow Quadrant

1. Understand the Four Quadrants:

The Cashflow Quadrant, developed by Robert Kiyosaki, is a framework that categorizes income earners into four distinct roles: Employee, Self-Employed, Business Owner, and Investor. Recognizing which quadrant, you’re in is the first step toward financial freedom.

2. Shift from Active to Passive Income:

The goal is to move from the left side of the quadrant (E and S), where you trade time for money, to the right side (B and I), where your money works for you through proper systems and investment.

3. Financial Education is Key:

Building wealth requires understanding how money works. Invest time in learning about financial literacy, investing, and business systems to make smarter decisions.

4. Build Systems, Not Jobs:

To reach financial freedom, concentrate on building systems that earn income independently of your active effort. This characteristic is a key feature of the Business Owner (B) quadrant.

5. Invest in Assets, Not Liabilities:

True wealth comes from acquiring assets, things that put money in your pocket (e.g., real estate, stocks, businesses). Avoid liabilities that drain your resources (e.g., excessive debt, depreciating items).

6. Overcome Fear and Take Risks:

Fear of failure and the unknown often holds people back. Take calculated risks and view mistakes as valuable learning experiences—they are crucial for personal growth and achieving financial independence.

7. Start Small, Think Big:

Transitioning between quadrants doesn’t happen overnight. Begin with small, actionable steps, like investing in education, starting a side hustle, or making your first investment, and gradually build toward bigger goals.

Conclusions

The Cashflow Quadrant is more than just a framework, it’s a mindset shift that can transform your financial future. By understanding where you are and where you want to be, you can take actionable steps to move toward financial freedom.

Remember, the journey from employee to investor isn’t easy, but it’s worth it. Begin with small steps, invest in your education, and surround yourself with individuals who motivate and push you. Financial freedom is attainable—take the first step now!

Which quadrant are you in, and what’s your first step toward financial freedom, share your thoughts in the comment below.

FAQs

1. What is the Cashflow Quadrant?

The Cashflow Quadrant, developed by Robert Kiyosaki, is a framework that categorizes income earners into four distinct roles: Employee, Self-Employed, Business Owner, and Investor. It helps individuals understand where their income comes from and how to achieve financial freedom.

2. Which quadrant is the best?

There’s no “best” quadrant—it depends on your goals. However, the Business Owner (B) and Investor (I) quadrants offer the greatest potential for financial freedom and passive income.

3. Is it possible to belong to multiple quadrants at the same time?

Yes! Many people operate in multiple quadrants simultaneously. For instance, you could be employed (E) and simultaneously invest in real estate (I).

4. Do I need a lot of money to become an investor?

No. You can start investing with small amounts, especially in areas like the stock market or mutual funds. Start investing early if possible and maintain consistency.

5. What steps should I take to transition from being an Employee to becoming a Business Owner?

Start by educating yourself about business systems and entrepreneurship. Consider starting a side hustle or small business while maintaining your job for financial stability.

6. How do assets and liabilities differ from each other?

An asset generates income for you—like rental properties or stocks—whereas a liability costs you money, such as car loans or credit card debt.

7. Is it risky to become a business owner?

Yes, there are risks involved, but with proper planning and education, you can minimize them. Start with very small investment and scale as you gain experience.

8. How can I generate passive income?

Passive income can come from investments like real estate, dividend-paying stocks, or businesses that run without your direct involvement.

9. What’s the first step to financial freedom?

The first step is to assess where you are on the Cashflow Quadrant and identify your financial goals. After that, concentrate on learning and making steady, incremental progress toward your objectives.

10. How long does it usually take to achieve financial independence?

The timeline varies depending on your starting point, goals, and level of commitment. With consistent effort and smart decisions, many people achieve financial freedom within 5–10 years.